How Expensive is a Low Credit Score When Getting a Mortgage

Dave Jensen June 12, 2024

Dave Jensen June 12, 2024

When it comes to getting a mortgage, it’s best to know exactly how expensive a lower credit score can be.

Broadcast news often reports a single mortgage rate as the national average for a 30-year fixed-rate conventional mortgage. It’s a decent gauge but what is not always reported is how good your credit score needs to be to get that rate. Also not reported is that those rates generally assume you’ll put down 20% of the purchase price as a down payment. Not easy for everyone.

There are many different types of mortgages. FHA, USDA, and VA are the most common alternatives to conventional mortgages. These require very low down payments (3.5% for FHA and 0% for USDA and VA).

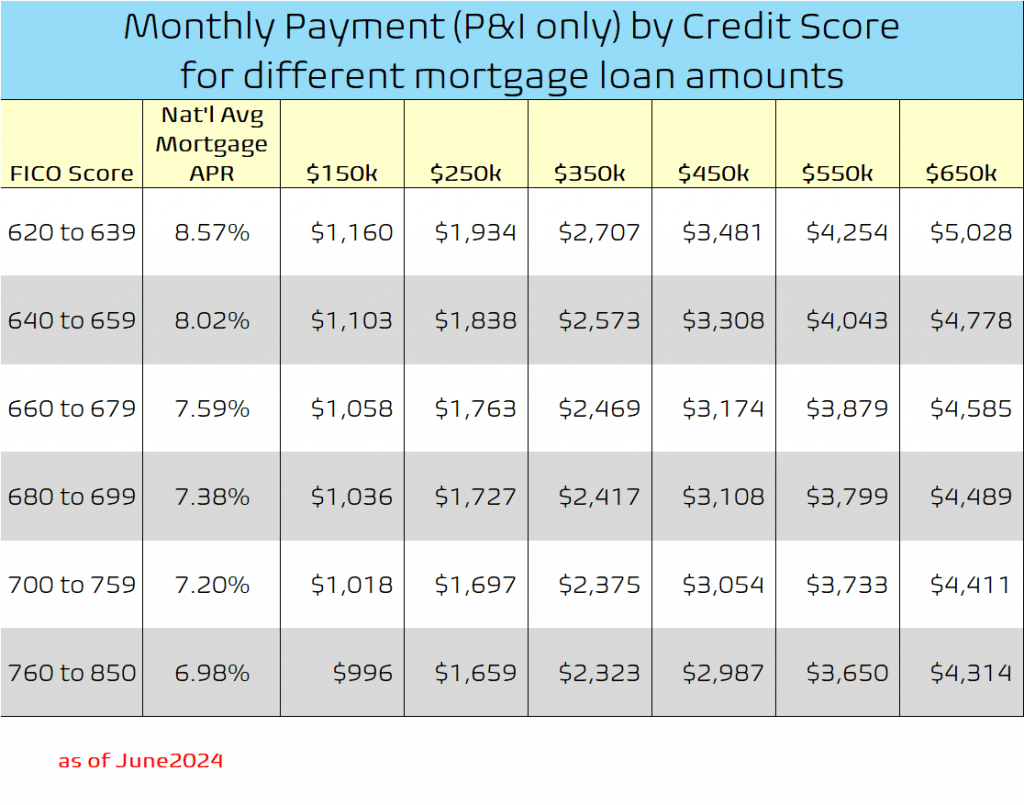

Data from credit scoring company FICO shows that the lower your credit score, the more you’ll pay for credit. That makes sense. But what is the actual cost?

Here’s a look at the different costs for a 30-year fixed-rate conventional mortgage.

That’s a difference of $198 per month. Not much, huh?

Across the life of the loan, you will end up paying over $71,110 more, just because you have lower credit.

It’s likely you’ll refinance or move before then, but why pay more at all if you don’t have to?

You can read more on this topic at this Business Insider site, and here’s another great resource on this topic. The Mortgage Reports

The rates change every day, and lately they change during the day.

Need more info? Reach out to me today. Call, text, or email.

The more you know, the better.

Stay up to date on the latest real estate trends.

The geometry of land value along Houston’s emerging Northeast corridors.

Most sellers focus on pricing. The real advantage comes from understanding when the right buyers are actually active.

Why the strongest offer isn’t always the one that protects your next move

In luxury real estate, timing matters far less than the structure behind it — and the structure begins with the plan.

Most stress comes from waiting to plan, not from the move itself.

Why homeowners in the 4–7 year window often discover misalignment too late

Leveraging experience and data to produce a solution that's a fit for you, your current and long-term goals. And it starts with our first conversation. Call today!

1335 Lake Woodlands Dr C The Woodlands TX 77380